The best culture and lifestyle news from Delaware

Provided by AGPUneasy Handshakes: Observations on Informal Settlements in Shareholder Activism

Few would expect even the most contentious and high-stakes activist-company disputes to end in something close to a handshake. Yet that is increasingly part of the story. Informal settlements now appear with enough regularity—and in sufficiently high-profile engagements—to make the paradox hard to ignore, even when a proxy contest intervenes along the way.

As used here, an informal activist settlement is a privately negotiated resolution of a disagreement between a company and an activist investor over strategy, governance, capital allocation, leadership, strategic alternatives, or other corporate matters. Unlike a formal settlement, it need not be embodied in a publicly disclosed written agreement. Instead, the outcome may be reflected in press releases and public filings announcing board appointments, related commitments, and statements of support from the activist.

Informal settlements are not new. Commentary in 2020 described them as an established, if selective, feature of the activism landscape, particularly in larger and more constructive engagements where the parties found enough common ground to avoid a formal cooperation agreement. More recent commentary likewise describes informal arrangements as workable where companies and activists can rely on a degree of strategic alignment and trust, allowing public commitments—such as board appointments, business reviews, or capital-allocation measures—to substitute for detailed contractual provisions. [7][8]

Since the introduction of the universal proxy card, settlement dynamics appear to have shifted. Recent commentary points to more settlements, faster settlements, a larger share of private resolutions, continued willingness by parties to settle rather than proceed to a vote, more operationally focused campaigns, and a more year-round activism environment, including off-cycle and “vote no” campaigns and more activists going public without extended prior engagement. [1][2][3][4]

In that setting, we reviewed 646 campaigns initiated in 2023, together with earlier campaigns that remained active enough to settle in 2023 or later. The empirical discussion below focuses on settlements that resulted in board representation, as those outcomes are the most consistently observable in public disclosures.

Between 2023 and April 1, 2026, 171 campaigns in the sample ended in settlements that included board representation. Twenty-nine of those settlements—17%—were informal under the definition above. By year, the share was 7% in 2023 (3 of 42), 20% in 2024 (11 of 55), 21% in 2025 (12 of 56), and 17% through April 1, 2026 (3 of 18). [10]

This pattern does not appear evenly distributed across the activist population. In our sample, 74 activists accounted for the 171 settlements that resulted in board representation, but only 18 accounted for all informal settlements. Nearly half of all informal settlements were attributable to just three activists, and one activist alone accounted for roughly 30% of the total. Among the 10 activists with the highest number of such settlements—each with between four and 21—five used informal settlements, while five did not use them at all. This concentration suggests that the use of informal settlements reflects firm-specific approaches at least as much as broader market conditions. [10]

The available settlement data suggests an evolution in how activism is practiced. Recent litigation and commentary also suggest that the structure of these settlements is receiving closer attention than it once did. Much of the discussion centers on two related themes: shareholder choice and board authority. The first concerns whether a settlement may, in practical effect, influence board composition before shareholders have had an opportunity to vote. The second concerns whether commitments made to an activist may be viewed as constraining the board’s ordinary decision-making or giving the activist an unusual degree of influence.

These themes are often discussed through three Delaware cases. Coster v. UIP is frequently cited in discussions of board action and electoral fairness. West Palm Beach Firefighters’ Pension Fund v. Moelis & Co. became an important reference point in commentary on how far governance rights may be shaped by contract, although the discussion around the case has continued to evolve following later developments. Miller v. Crown Castle brought similar issues into the activist-settlement context. There, Crown Castle co-founder Theodore B. Miller, Jr. and Boots Capital challenged Crown Castle’s cooperation agreement with Elliott after the company granted Elliott board seats and related governance commitments. The claim focused attention on whether a settlement reached shortly before the annual meeting, and in the context of questions about the activist’s economic exposure, could be seen as improperly affecting the shareholder vote.

Taken together, these cases do not appear to establish a single rule for settlements. They do, however, help explain why recent commentary has focused more closely on settlement structure itself. The discussion increasingly asks whether a settlement preserves the board’s ability to exercise its judgment, ties influence to a clear and transparent economic stake, and respects the role of shareholders in the electoral process. [5][6][9]

As a result, both the activist playbook and the scope of company concessions may increasingly be shaped by tradeoffs across several variables: tolerance for litigation risk, choice of investment instruments, willingness to depart from ordinary governance structures, timing relative to the proxy process, the contractual flexibility that may come from avoiding a formal agreement, and the practical benefits of lower cost, less process, and greater speed. [4][5][6]

Our data suggests that informal settlements are reached more quickly on average, although the difference narrows once longer-running campaigns are excluded. For campaigns producing board outcomes between 2023 and 2026, timing is measured from first public disclosure of the campaign to settlement. Excluding campaigns exceeding 365 days, informal settlements were reached in 79 days on average, compared with 88 days for formal settlements. The gap was wider in 2024 and 2025, where informal settlements were reached 38 and 25 days sooner, respectively. [10]

Speed, however, does not appear to be matched by equally clear differences in other observable features of the settlement. Apart from the contractual provisions that by definition distinguish formal agreements—such as standstills, minimum ownership thresholds, and similar clauses—informal settlements do not appear materially different from formal ones in the other dimensions we examined. This is true of seasonality, where the annual curve for informal settlements broadly tracks that of formal settlements, and of activist principal representation on boards, where at least one fund employee or principal joined the board in roughly one out of every three settlements in both subsets. [10]

On the other hand, informal settlements accounted for 17% of settlements but only 13% of total board seats won, implying an average of 1.4 seats per settlement, compared with 1.9 for formal agreements. Greater board representation, in this sample, appears more often to have been achieved through formal settlements. [10]

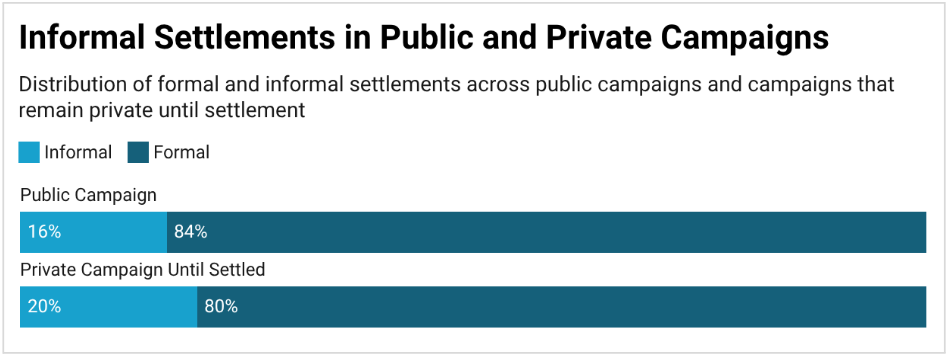

A related point concerns private engagement. Our data shows a modestly higher share of informal resolutions among campaigns that remained private until settlement and were disclosed only at that stage, though not by a margin that supports a stronger inference. This direction is consistent with prior commentary observing more private settlements in the universal-proxy era and describing constructive, trust-based engagement as a setting in which informal arrangements may be workable. [1][4][7][10]

One possible explanation—though not something the data can establish—is that where activists did not need to escalate publicly and companies engaged constructively, the parties may have developed sufficient trust and alignment to dispense with a detailed public agreement. Another possible variable is the nature of the activist’s economic exposure: commentary surrounding Miller has highlighted the scrutiny that may arise when governance rights are granted to investors whose exposure may be held in part through derivatives or other less transparent instruments. At this stage, both points are better framed as hypotheses for further empirical work than as conclusions. [5][6]

Sources

[1] Pat Tucker, Garrett Muzikowski, and Sean Lange, What Settlement Data Says About the Evolution of Activism, Harvard Law School Forum on Corporate Governance (July 15, 2024).

[2] Neil Whoriskey, Dean Sattler, and Scott Golenbock, Activism in the 2024 Proxy Season and Implications for 2025, Harvard Law School Forum on Corporate Governance (Mar. 14, 2025).

[3] Ele Klein, Brandon Gold, and Samuel Dayan, Shareholder Activism Developments in the 2025 Proxy Season, Harvard Law School Forum on Corporate Governance (June 18, 2025).

[4] Elizabeth R. Gonzalez-Sussman, Ron S. Berenblat, and Roy Cohen, As Activism Becomes a Year-Round Sport, Possible Regulatory Changes Could Impact Both Activists and Companies, Harvard Law School Forum on Corporate Governance (Feb. 3, 2026).

[5] Jennifer O’Hare, Why Boards Should Think Twice Before Entering into Cooperation Agreements With Activists, CLS Blue Sky Blog (Sept. 19, 2024).

[6] Jim Woolery, From Moelis to Miller: How to Settle with Activists, Harvard Law School Forum on Corporate Governance (Mar. 26, 2024).

[7] Elizabeth R. Gonzalez-Sussman, Ron S. Berenblat, and Dara J. Ferguson, Should Boards Be Wary of Informal Settlements With Shareholder Activists?, Harvard Law School Forum on Corporate Governance (Apr. 14, 2026).

[8] Chelsea Naso, Informal Settlements, ESG Issues To Permeate 2020 Activism, Law360 (Jan. 1, 2020)

[9] Coster v. UIP Cos., Inc., 300 A.3d 656 (Del. 2023); Moelis & Company v. West Palm Beach Firefighters’ Pension Fund, No. 340, 2024 (Del. Jan. 20, 2026), rev’g West Palm Beach Firefighters’ Pension Fund v. Moelis & Co., C.A. No. 2023-0309-JTL (Del. Ch. Feb. 23, 2024); Theodore B. Miller, Jr. and Boots Capital Management, LLC v. P. Robert Bartolo, et al., C.A. No. 2024-0176-JTL (Del. Ch. Mar. 8, 2024) (transcript ruling on motion for expedition).

[10] Data: DEF 14 Inc. For purposes of this article, an “informal settlement” is a settlement with board representation for which no signed cooperation agreement was publicly disclosed, but public disclosures reflected board appointments, related commitments, and activist support. Timing is measured from first public disclosure of the campaign to settlement announcement or signing. 2026 data through April 1, 2026.

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.